Is China’s industrial policy working?

Thanks to China’s industrial policies, notably the “Made in China 2025” plan launched in 2015, a large amount of resources has been used to promote home-grown innovation and self-reliance in technology in order to reduce China’s dependence on the West. The plan covers 10 key industries, including information technology (IT), robotics, new energy and biotech.

To this end, China has significantly increased spending on research and development (R&D). While R&D spending accounted for 2% of gross domestic product in 2015, it had risen to 2.6% by 2023, approaching the OECD average of 2.7%. China was already spending more on R&D than the EU (2.1%), but still less than the US (3.5%). In absolute terms, adjusted for purchasing power, China’s R&D spending accounted for 95% of that of the US. In contrast, the EU only reached 61% of the US level.

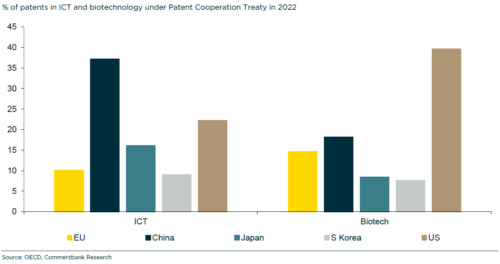

Looking at the number of patents filed worldwide, China is ahead of the US, with a share of 27% in 2022. Also, China has caught up strongly in patents on information and communication technology (ICT) and biotechnology (Exhibit 1).

According to a study by the Australian Strategic Policy Institute (ASPI), China is the leader in 37 of 44 technologies evaluated; often publishing more than five times as much high-impact research as its closest competitors in areas such as advanced manufacturing and materials, artificial intelligence (AI) and computing, energy and environment, quantum computing, biotechnology, defence, space and robotics.

A separate study by the Information Technology & Innovation Foundation (ITIF) shows that China is the global leader in electric vehicles (EV) and is close to the world leaders in AI, robotics and quantum computing.

Exhibit 1: China leads in ICT patent filings

Yet the economic value created has been limited

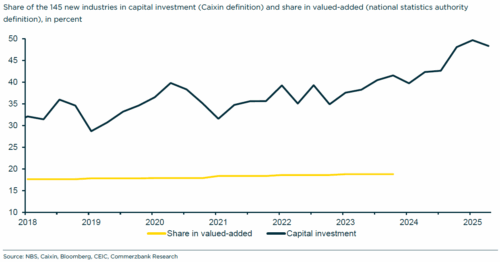

Given China’s enormous investments in new industries, in theory, these industries should outperform the rest of the Chinese economy. But this is hardly the case. The share of these industries in total value-added has not risen significantly, although their share of capital investment has increased considerably (Exhibit 2).

Exhibit 2: New economy’s share of capital investment rose but not its share of total value-added

Value added—defined as the difference between a company’s sales and the value of intermediate inputs—is likely to suffer most from falling sales prices due to overcapacity and the resulting ruinous competition.

There are too many companies chasing too little demand. This has led to a problem of “involution”, which has been vastly reported in both Western and Chinese media recently. This refers to a self-defeating cycle of fierce and often unproductive hyper-competition. Producer prices in industry have been falling for almost three years, and 23% of Chinese industrial companies are now reporting losses.

The fact that such overcapacity is seen has a lot to do with the role of local governments. Since China is a vast country and each province has different resources and cultures, the central government in Beijing often delegates the implementation of economic policy to local governments. Local governments have to achieve their own GDP growth targets as well as innovation targets, among other policy goals assigned by Beijing.

Local officials must largely meet the targets if they want to advance their careers. This is why they promote companies from the new industries. Imagine every local government striving to have its own manufacturer of electric vehicles, for example. This leads to overinvestment and overcapacity. In reality, this is not only happening in the EV industry but is broad-based across the economy.

In addition, local governments must also ensure sufficient tax revenues. Since value-added tax (VAT) and corporate income tax account for over 60% of general tax revenues, they cannot afford to lose large taxpayers, so they continue to promote these companies even if the prospects for decent profits are slim.

However, industrial policy is likely to continue

China is likely to continue its industrial policy in the medium term (five years). This is because home-grown innovation and self-reliance in technology are considered a top priority for the leadership. Compared to this policy goal, economic efficiency is secondary. From a medium-term perspective, China is willing to pay a price for innovation in the form of overcapacity and market distortions—especially since it is difficult for the government to control the production and prices of private companies and to closely manage local governments.

In the long term, beyond the next five years, however, it will become increasingly difficult for China to stick to its current industrial policy. The cost of innovation gets steeper for achieving further technological advances, especially since there are no “unlimited” resources available to subsidise the new industries. Government debt has already risen significantly (over 120% of GDP in 2024 based on our broad measure) and is likely to increase further due to the shrinking working population.

To conclude. China has displayed some spectacular rise in innovation, driven by the government’s industrial policy in recent years. But this has not yet translated into higher value-add of the “new industries” relative to the whole economy. The way that the industrial policy is implemented by local governments causes the infamous problems of “overcapacity” and “involution” or ruinous competition. While Beijing is set to rein in these problems in the near term, China will continue its industrial policy because Beijing sees innovation and self-reliance of technology as the top economic priority. But the innovation model will be challenged in the long run because state resources are limited by its fiscal constraints amid demographic challenges.

About the author

Tommy Wu is a Senior Economist at Commerzbank AG, currently based in Singapore. He covers macroeconomic research of China’s economy. Prior to joining Commerzbank, Tommy was a lead economist at Oxford Economics, where he covered Greater China as well as the rest of the Asia-Pacific region. Tommy also spent several years as an economist at the Hong Kong Monetary Authority. Tommy is a frequent contributor to international media and has been invited as a keynote speaker and panelist at various professional events. Tommy holds a PhD in Economics from Queen’s University, Canada.